Summary

- Questions are being asked of direct lenders about when a company underperforms and requires a restructuring; are lenders ready to “take the keys”?

- First and foremost, the main goal of lenders is to avoid such a scenario as much as possible with rigorous credit selection (to choose companies and private equity sponsors less likely to underperform) and strict portfolio monitoring (to address underperformance as soon as possible).

- However, when a financial restructuring is required, investing with the right partners, experience and proactivity are crucial. A collaborative approach and expertise in this area can maximise recoveries (and therefore returns for investors).

Introduction

Given today’s economic headwinds, it is natural for investors to increase their focus on the health of direct lenders’ portfolio companies. Over the last two years, borrowers have faced and continue to face economic and geopolitical challenges, with many predicting an increase in default rates. Whilst this could be seen as a “normalisation” in default rates after a period of lower defaults supported by very low interest rates, nonetheless it is a challenge for direct lenders whose alpha stems from the ability to avoid defaults and minimise losses compared to the market. This may be more difficult for lenders who have not managed portfolios during a significant downturn, with many direct lenders established during the benign environment following the Great Financial Crisis of 2007/2008 (“GFC”).

Avoiding Portfolio Underperformance

Credit Selection

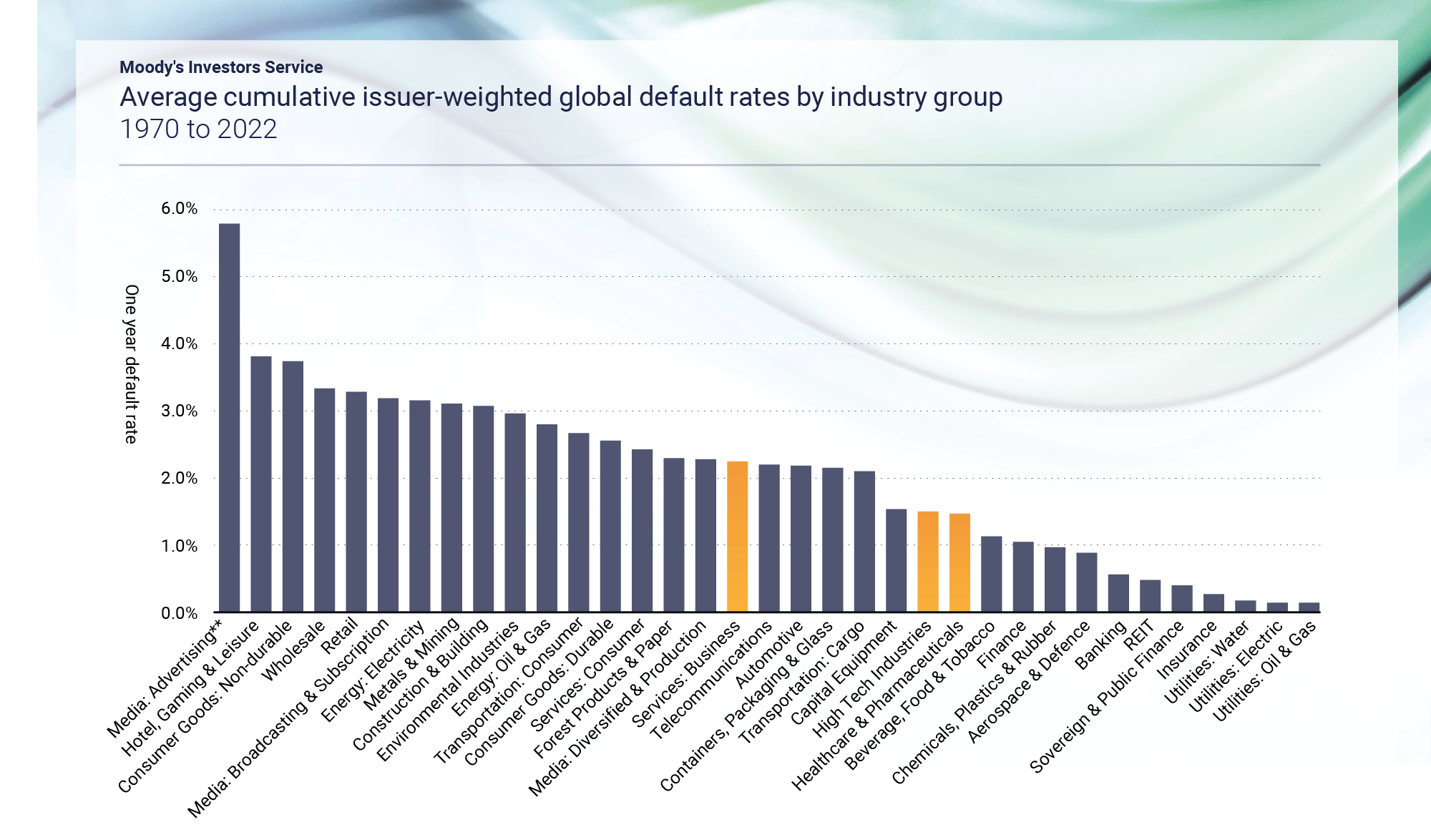

The importance to direct lending of rigorous credit selection cannot be stressed enough. Many times, a company’s industry or credit characteristics are a factor in underperformance. In MV Credit’s view, in part based on experience of portfolio companies invested into prior to the GFC, some industries, such as household durables, are more correlated to economic cycles and cannot sustain highly leveraged capital structures in a downturn. Other “red flags” MV Credit looks for in the due diligence process include exposure to raw material price fluctuations and raw commodity prices, as well as business models that are capex intensive or have high fixed costs.

MV Credit originates opportunities with this in mind, exercising caution towards certain industries and avoiding companies with weaker credit fundamentals. The graph below1 shows data on market default rates from 1970 to 2022, with the three industries highlighted making up a significant portion (over 70%2) of MV Credit’s current portfolio.

In addition, in comparison to smaller companies, the upper mid-market space can have a better risk-return profile. Upper-mid cap companies usually have more pan-European or even globally diversified revenue streams, and are less reliant on a single geography, product or customer compared to small-cap companies. Therefore, they are less sensitive to changes to the political, economic or legislative environment of a single geography, which mitigates country specific and geopolitical risks.

Partnering with the Right Equity Owner

MV Credit estimates that since 2020 it has originated opportunities for its direct lending platform across companies owned by more than 170 different private equity sponsors. It has retained selectivity however and has partnered with just under 303 in its current portfolio. Looking back, MV Credit has found most of the private equity sponsors it has worked with proactive and supportive of borrower companies in instances of underperformance. MV Credit believes that partnering with the “right” equity owner, in particular a reputable private equity sponsor, is key to downside protection and can help minimise the impact of credit losses.

An experienced and collaborative private equity sponsor should be relied on to manage borrower companies effectively, able to execute the initial investment strategy (by growing the business) and proactively address any unexpected problems that may arise. Sponsors’ management can be a factor in what goes wrong for a borrower company, for example if they lack direction for the company (as a result of not following through with the initial thesis) or if they are less proactive in addressing issues early on. The sponsor (and management) should act early to make changes to a borrower company in times of stress or underperformance.

Based on experience, MV Credit has consolidated and institutionalised relationships with the “right” private equity sponsors. Partnering with private equity sponsors is key to MV Credit’s origination and allows it to monitor company performance through close communication with the owner. If a company underperforms, an institutional relationship between MV Credit and the sponsor (as well as other lenders) can help facilitate an outcome and increase the likelihood of negotiations of a financial restructuring being consensual and balanced between lenders and equity holders. Non-consensual restructuring processes based solely on an aggressive use of pre-insolvency or insolvency regimes can be expensive in execution and remediation, and lead to further value destruction.

Experience Matters If Things Go Wrong

Despite stringent credit selection and partnering with supportive private equity sponsors, direct lenders must be realistic that some portfolio companies will go on to underperform expectations, particularly during a downturn. This can result in restructurings and consequentially changes to the terms of the original loan agreement in several ways, including altering the debt pricing profile, extending its contractual maturity, altering a company’s capital structure (including through partial or full debt for equity swaps), and allowing new money injection(s). Restructurings in private debt markets are different in nature to those in public markets, with a much smaller, contained group of lenders typically negotiating them directly with a similar group of shareholders. When the equity investors have a collaborative mindset, reaching balanced agreements is quicker which ultimately preserves more value for all stakeholders. In addition, consensual restructuring negotiations avoid much of the unnecessary and unhelpful public press coverage which could damage company value, for example with clients or suppliers moving elsewhere.

MV Credit has been involved in restructuring situations, most of which date back to the GFC. Whilst restructurings have different circumstances and involve a range of key players; experience demonstrates the ways in which a direct lender can seek to safeguard their investment:

- Identify problems early. MV Credit advocates an approach of “healthy paranoia” towards all portfolio companies and has established monitoring processes aiming to pick up early warning signals of underperformance. A key part of this at MV Credit is its independent Credit Monitoring Team, which systematically monitors each portfolio company alongside the Deal Team.

- If there are signs of underperformance, it’s essential to proactively start discussions early with the private equity sponsor and other stakeholders, even informally. This is crucial to preserving the value of a company and ensuring its future, increasing the likelihood of a successful business turnaround.

Once in a restructuring, the ultimate agreement is typically based on full consent by the lender(s), or a majority of lenders where there is more than one. Working collaboratively, maintaining dialogue with stakeholders, and aiming for a consensual solution is usually the best way to minimise credit losses and ensure that trustworthy relationships are maintained. MV Credit frequently adopts a leadership role in restructurings, often playing an important role in formal or informal "Steering Committees", which are led by a group of the largest or most relevant lenders typically commanding a combined majority of any given debtor class. This approach led to substantially lower loss rates than the market for MV Credit’s 2006 vintage subordinated strategy, which had a loss rate of 1.6% compared to the estimated market rate of 2.5%4.

The European lending market is different from the US. Managers lending in Europe should ensure they understand and have experience in lending across the different jurisdictions so that they can tailor restructuring approaches to improve outcomes. Managers should also be ready to offer flexible solutions, including providing additional “follow-on” money to companies where relevant. Many restructurings are triggered by liquidity issues, so having the ability to inject new money can help support the portfolio company and improve the outcome for the lender.

With the increase in club deals (where a handful of lenders come together to finance a company), observed over the past few years5, some wonder how direct lenders in a club can ensure they are well represented in a restructuring, and whether they can exert “control”. However, historically club restructurings have been more tested than those involving a single lender, and being in a club of lenders still enables a direct lender to play an active role through Steering Committees, with the largest lender not necessarily taking the lead in negotiations. Additionally, sole lenders in a restructuring may end-up becoming the lender of last resort by default. In transactions with several lenders, the new money requirements could be either spread among lenders or be optional should one of the lenders not be convinced of the cost/benefit of the additional new money investment.

Conclusion

It is the difficult task of investors to determine which direct lender they should partner with. There are information barriers to assessing the private direct lending market compared with public markets. For example, it may not widely be known that a company is being restructured until it is publicly reported that a lender has taken ownership of it. A further challenge to forming a conclusion is that the current economic environment is the first major test of the direct lending space.

Ultimately, track record data and past performance is a very useful indicator of a manager’s calibre. MV Credit sees historic loss rates as an important measure of performance, with loss rates a fundamental driver of returns in debt investing. Low loss rates matter, whether achieved through credit selection, active monitoring or restructuring expertise.

Footnotes

1 Source: Moody’s Annual Default study 2023. Exhibit 43: Average cumulative issuer-weighted global default rates by industry group, 1970-2022. Data shown is 1 year default rate. Industry category “Media: Advertising**” has been abridged from “Media: Advertising, Printing & Publishing”.

2 As of 30th June 2023 based on MV Credit unrealised investments across its strategies. Sector classification derived by MV Credit.

3 As of 30th June 2023 based on MV Credit unrealised investments across its strategies.

4 Source: MV Credit, as of 30th June 2023. Average loss rate is for all MV Credit realised investments since inception, excluding equity investments, for the given strategy. Loss rate calculated as average of loss rates for the given strategy each year, where each loss rate is total amount lost over total asset value. Based on year of investment default. Market loss rate is based on Moody’s Global Annual Default Study 2023. Average loss rate is based on yearly speculative-grade default rates and 2nd Lien Bank Loan volume-weighted recovery average (1983-2022) between 2005 – 2017.

5 Sources: AIMA “Financing the Economy 2022”, LCD “syndicated deals increase as direct lenders grab bigger share”, 2021.